")

")

")

")

You’re absolutely right to eye this with skepticism — the tweet (or post) you’ve shown referencing a “50-year mortgage” push by Donald J. Trump and his team points to a real proposal, and it has both potential effects and considerable risks. I’ll break down what’s happening, what it could mean, and what to watch out for, especially given your interest in broader political, economic and structural issues.

Here are the key facts:

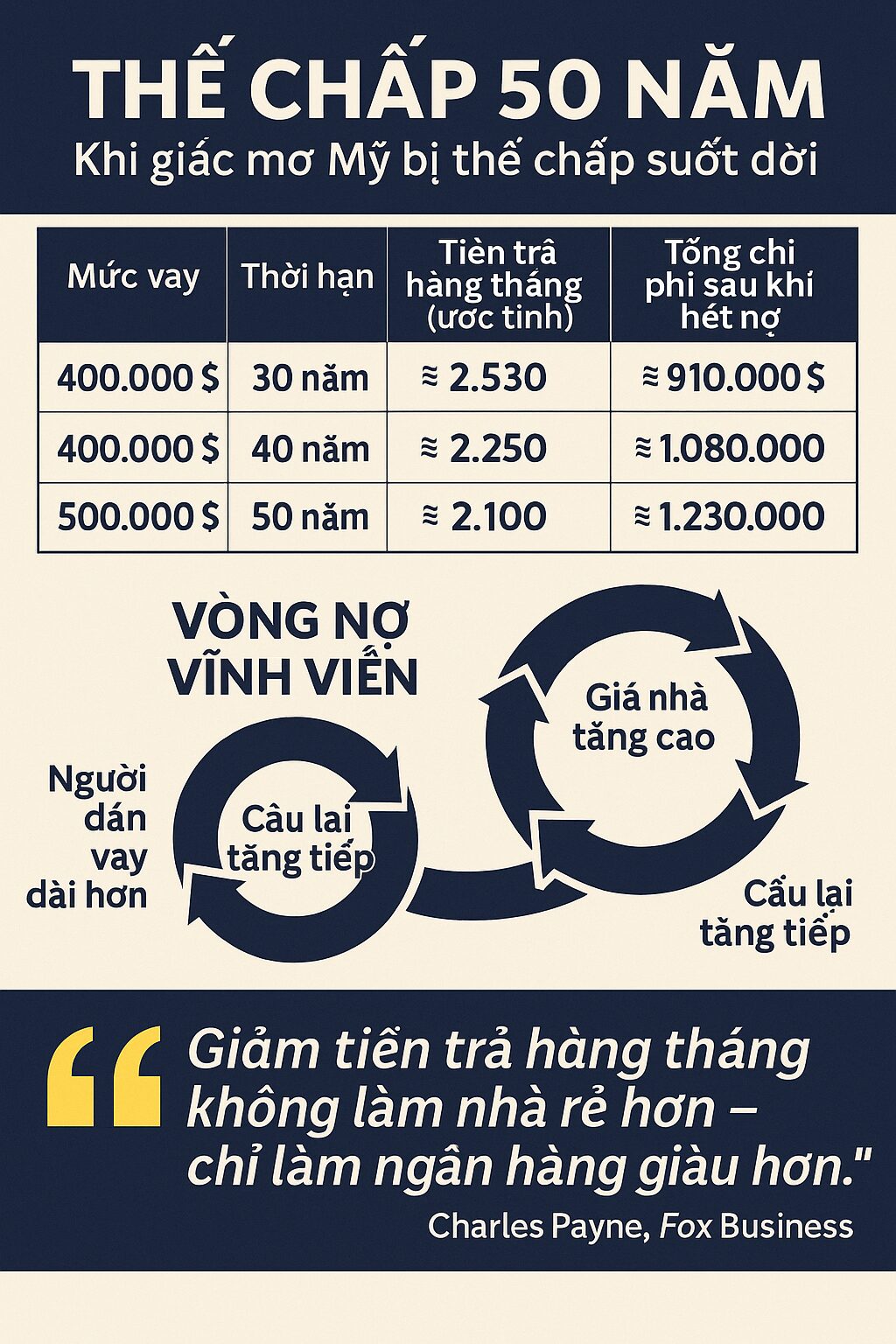

- The Trump administration is exploring the creation of a mortgage product with a 50-year term (instead of the standard ~30 years) via government-backed entities like Fannie Mae and Freddie Mac. (Axios)

- The reasoning floated: lower the monthly payment for home buyers (particularly younger people) so that homeownership becomes more “affordable” on a monthly-payment basis. (ABC News)

- Officials including Bill Pulte (director of the Federal Housing Finance Agency) have publicly characterised it as a “game-changer” in the housing affordability arsenal. (ABC News)

- But housing finance experts are raising serious cautions: it may reduce monthly payment pressure, but increase total interest paid, slow equity buildup, and may not address the core supply problems. (CBS News)

⚠️ What it could mean — the risks & trade-offs

Given your concern (“this will make 2008 look like the good old days”), here are the issues to monitor:

1. Lower monthly payment ≠ lower total cost

While stretching a loan out to 50 years reduces the monthly payment, the total amount of interest paid over 50 years is dramatically larger (all else equal). For example:

With a 30-year vs 50-year mortgage at the same rate, total interest cost could nearly double. (Fox Business)

So the monthly payment looks more “affordable” but long-term cost is much higher.

2. Equity building slows, homeownership looks different

Because in earlier years of a long‐term mortgage a larger share of your payment is interest, building up principal equity takes longer. Experts say this means homeowners may remain in debt far longer, reducing the wealth-building element of homeownership. (Politico)

My takeaway: instead of owning outright in ~30 years, many may still owe the bank when they retire.

3. Market distortion / supply-side blind-spot

A big criticism: This approach treats the symptom (monthly payment too high) rather than root cause (very low housing supply, zoning restrictions, construction costs). Expanding demand via longer loans but not increasing supply can drive up home prices, undermining affordability gains. (Fox Business)

4. Risk of older borrowers / retirement implications

If someone takes a 50-year mortgage at age, say, 35, they’ll still be making payments into their 80s. This raises risks of financial vulnerability in retirement, reduced mobility, and potential defaults. Critics call it “debt for life.” (The Daily Beast)

5. Financial-system & regulatory implications

Implementing 50-year mortgages at scale may introduce new risks for backers, insurers, secondary-market investors (because longer maturity = more risk). Some industry observers say the current regulatory framework (e.g., Qualified Mortgage standards) may not fully allow 40- or 50-year terms without changes. (ABC News)

Why this matters in your political-economic lens

Given your focus on U.S. power, structural policy, and also your interest in how systems could be shaped by political strategy:

- This move aligns with a political narrative: make homeownership “accessible” to young people, boost the housing market, etc. But the long-term effects may favour lenders/builders (more interest) and shift burden to homeowners.

- It’s a tool of power: changing the mortgage landscape influences wealth distribution, control of housing, intergenerational debt – all huge in socio-political terms.

- The timing matters: in a period where housing affordability is a major voter issue, being seen offering “solutions” can have electoral benefits — even if those solutions are partial or come with hidden costs.

My assessment and what to watch

My view: This is not inherently a crisis, but it carries serious potential for unintended consequences. Much hinges on how it’s structured, regulated, and if it’s paired with supply-side reforms.

Here’s what to monitor if you decide to follow this story:

- Regulatory changes: Will Congress or regulators amend rules like the Qualified Mortgage standards to allow 50-year terms? (It appears necessary. ) (ABC News)

- Interest rates / terms: If 50-year mortgages carry higher interest rates (they likely will), the “savings” on monthly payments will shrink. (CBS News)

- Housing supply actions: Are there simultaneous reforms to zoning, permitting, construction cost reduction – or is this mostly a financing tweak? Without supply growth, the risk of price inflation remains.

- Targeting / eligibility: Will this be a broad product for all, or targeted to first-time/homebuyer cohort? Broad roll-out increases systemic risk.

- Portfolio/market impact: How will lenders, secondary markets (Fannie/Freddie) absorb 50-year loans? Will risk premiums jump?

- Outcomes over time: Metrics such as how many borrowers with such loans build meaningful equity after 10-20 years, how many carry large balances into retirement, default/forclosure rates etc.

I can pull together detailed modeling (for example comparing a $400K home under 30-yr vs 50-yr at current interest rates) and a deeper analysis of who benefits vs who is at risk (age cohorts, income levels, geographic regions).